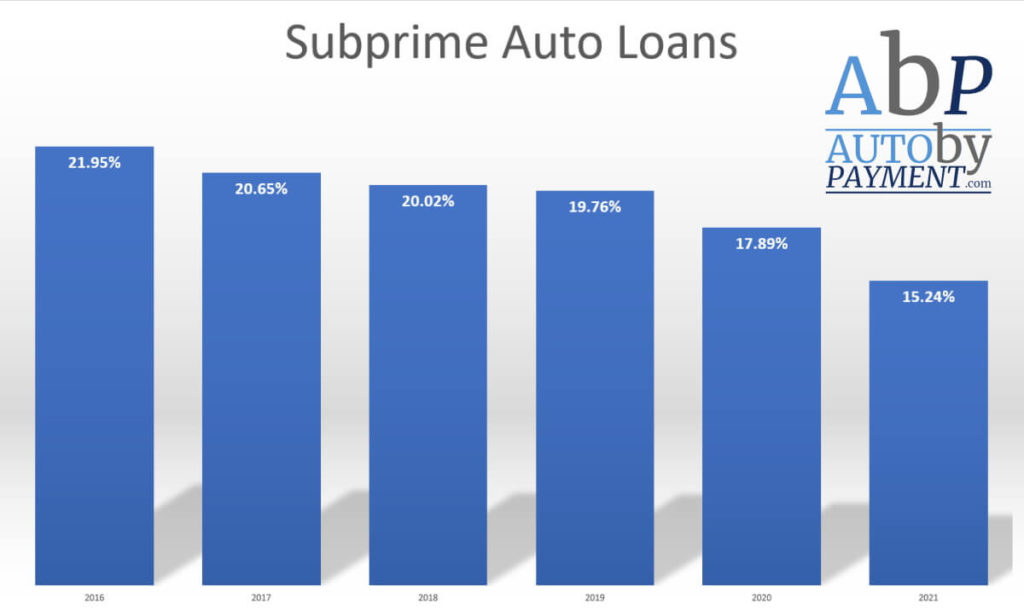

As reported by Experian, new and used auto loans through banks and finance companies for people with bad credit have decreased 30.56% in the last 5 years. In 2016 auto financing for people with credit scores under 600 accounted for 21.95% of all auto loans. In 2021 only 15.24% of the auto loans generated were from people with credit scores under 600. There are several reasons why this is happening. Before we look at what is causing the decrease in auto loans for people with bad credit let’s take a look at the two lender parameters that drive auto loan approvals.

When applying for an auto the two major factors that banks and finance companies evaluate are the Loan to Value Ratio (LTV) of the vehicle and the Payment to Income Ratio (PTI) of the applicant. For lower credit scores favorable LTV ratios fall below 110% and PTI ratios fall below 12.5%.

What Affects the LTV Ratio?

LTV is defined at the Total Loan Amount divided by the Vehicles value. For new cars most lenders use the Invoice Price of the vehicle. The Invoice Price set by the manufacturer is a fixed price for the specific vehicle and model year. It does not fluctuate based on inflation or market conditions. During an inflationary period it is likely that the Invoice Price will increase year over year.

When the Market Value or Price increases and the Value remains fixed, the LTV ratio will increase. Conversely, when a larger down payment in the form of cash or new car rebates is applied to a loan the LTV will decrease. In other words the Down Payment and Price will have a positive or negative effect on the LTV Ratio.

What Affects the PTI Ratio?

PTI is defined as the Monthly Loan Payment divided by the Gross Monthly Income of the borrower. Monthly payments are based on the amount borrowed, the interest rate, and the number of payments to repay the loan.

Similar to the LTV ratio, the Market Price and Down Payment have the same effect on the PTI ratio. The added components here are the interest rate, repayment term, and income. If the loan amount remains the same the PTI ratio will increase as interest rates rise and repayment terms decrease. Conversely, if wages rise the PTI ratio will decrease.

What is Causing the Decrease in Subprime Auto Loans?

In short, the supply shortage, gas price hikes, and rising interest rates are contributing to lower originations of auto loans for people with bad credit.

The Supply Shortage

The supply shortage is likely the largest contributor to the decrease in subprime auto financing. With a shorter supply, manufacturers are offering fewer incentives to move their inventory. While most people with lower credit scores do not qualify for low rate auto finance deals offered by the OEMs captive finance companies they do qualify for cash back rebates. A healthy cash back rebate will lower both the LTV and PTI and increase the chances of approval for subprime borrowers.

With the supply shortage many dealers have marked-up their new cars above the MSRP. At the same time the Invoice Price on these vehicles has remained the same. Simple math dictates an increase in price while the lender value remains the same will cause an increase in the LTV and fewer approvals for those with a poor credit rating.

Gasoline Prices

As fuel prices increase there is an increased demand for higher MPG cars. More often than not, higher MPG cars are less expensive than higher MPG cars. For example a small to midsize sedan will typically have a much lower price and higher MPG than a large or midsize SUV. As the demand for these lower price high MPG vehicles increases the market value increases as well.

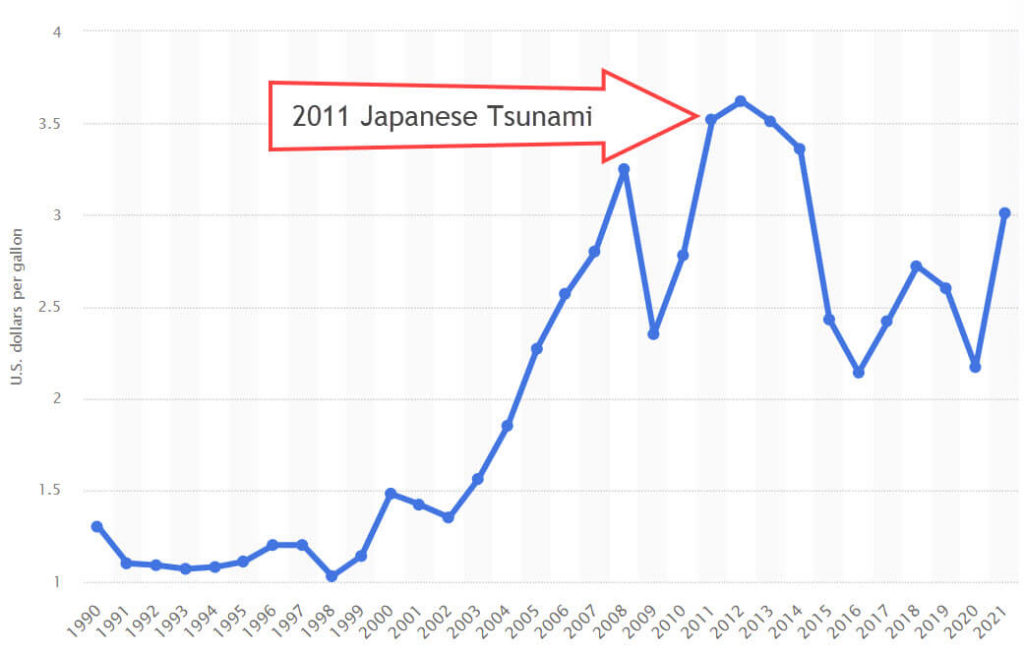

We saw something similar back in 2011. When the Japanese tsunami shortened the supply of lower cost fuel efficient vehicles. From 2011 to 2013 the demand for fuel efficient cars increased due to high gasoline prices. At that time fewer vehicles were available due to the tsunami. The price of gasoline is a lagging indicator for subprime auto loan generations. As gasoline prices increase so does the demand for lower priced higher MPG cars, with higher prices and fewer low cost cars available the LTV and the PTI for borrowers increase.

Interest Rates

For the first time since 2018 the FED announced an interest rate increase. They also stated that a few more increases will come in 2022. While rates for great credit borrowers decreased by 0.56% in 2021, deep subprime auto loan rates increased by 0.08% in 2021. An increase in interest rates will increase the monthly loan payment amount as well as the PTI ratio.

To keep the PTI ratio in check with the lender, poor credit consumers will have to increase their down payment amount or purchase a less expensive vehicle. Not an easy task with fewer rebates and decreased low cost inventory due to the supply shortage and raising gas prices.

Some Good News

It’s not all gloom and doom for subprime auto shoppers. Last Friday CNN, FOX, and CNBC reported that starting July 1, 2022 Equifax, Experian, TransUnion will remove the majority of medical debts from consumers’ credit reports. This action will increase the credit scores for millions of Americans with derogatory medical debt on their credit reports, a good portion of which will be moved from the subprime credit tier to the near prime or the prime credit tier.

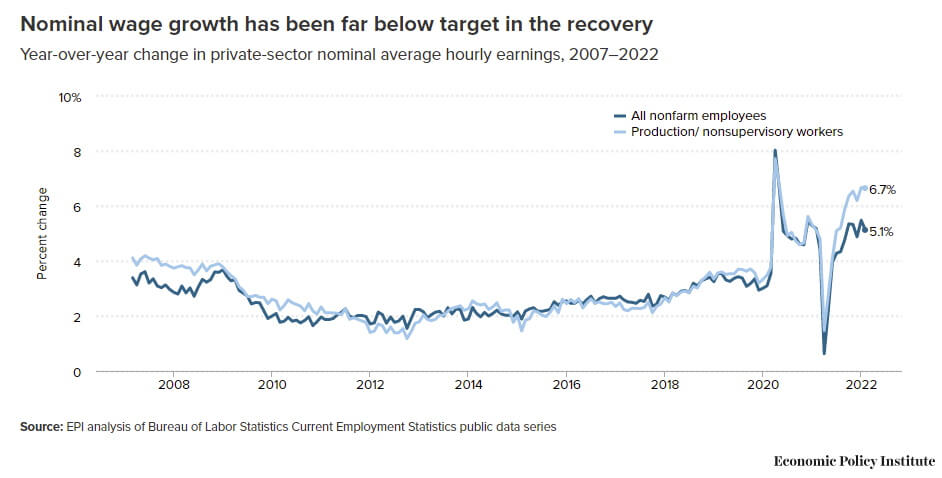

There is also some good news on the wage front. Since December of 2020, nominal wages and salaries were up 4.5 percent, the fastest increase since 1983. While still not keeping pace with inflation an increase in wages will decrease the PTI ratio and have a positive effect on the approval rate for bad credit car shoppers.

Each month we review vehicle prices and OEM rebates to select the best new cars for people with bad credit. Our list contains the new car models which are easier for consumers to obtain an auto loan approval based on the vehicle price and available rebates.

Our 2022 Outlook

We expect the trend of lower inventories, fewer new car incentives, higher prices and interest rates to continue in 2022. We recommend that consumers with lower credit scores wait until 2023 before trying to obtain a new auto loan. Between now and then they may get a bump on their credit score, especially if they have medical collection accounts. It also allows time to improve their income in a hot job market as well as improve their credit score above 600.

About Us

AutoByPayment.com offers accurate estimates of new car loan payments based on self selected credit score, current rebates, down payment, and trade equity or negative equity, without customers having to provide their personal identifying information such as email and phone.