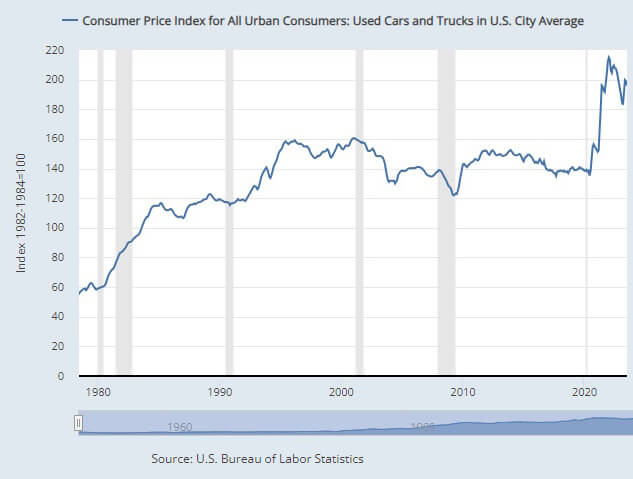

When discussing the automobile market of the recent past, one cannot overlook the significant price surges for both new and used cars. Specifically, the period between August 2020 and March 2023 saw unprecedented spikes in prices, with used car values peaking in February 2022 and new car prices reaching their zenith in March 2023. This pricing behavior had severe repercussions on those who made purchases during these timeframes, especially if they used minimal or no down payments. One of the most pertinent repercussions is negative equity.

Understanding Negative Equity

To start, let’s understand what negative equity means. When you owe more on a loan than the underlying asset (in this case, a car) is worth, you’re said to have negative equity in the vehicle. It’s sometimes referred to colloquially as being “upside down” on a loan.

Why The Timing Matters

Purchasers in the aforementioned time frames are especially vulnerable to negative equity for a variety of reasons:

- Inflated Purchase Prices: Cars bought during these peak price periods were secured at a premium. Once market prices begin to normalize or decline, the value of these vehicles can decrease sharply, even if the car itself remains in excellent condition.

- Depreciation Curve: Cars, especially new ones, depreciate rapidly in the first few years. Buying a new car at its peak price and coupling that with the natural depreciation can result in the vehicle’s value plummeting below the remaining loan balance.

- Low to No Down Payments: A substantial down payment helps in offsetting the initial hit of depreciation. However, with minimal or no down payment, buyers begin their ownership with almost the entire loan value to pay off. This further widens the gap between owed amount and the car’s worth, exacerbating the negative equity situation.

The Double Whammy of Rising Prices

The simultaneous increase in both used and new car prices during closely aligned periods exacerbated the situation. Those who bought a used car in the hopes of avoiding the steep prices of new cars were still paying a premium. If they then hoped to switch to a new vehicle as new car prices started to rise, they were hit twice: first, by the decreasing value of their used car, and second, by the increased price of new cars.

Why Did Prices Surge?

Multiple factors contributed to the soaring prices:

- Supply Chain Disruptions: The global pandemic and other geopolitical issues disrupted supply chains, creating shortages in car parts, particularly semiconductors.

- Increased Demand: Stimulus checks, pent-up demand after lockdowns, and a reluctance to use public transportation due to health concerns boosted car purchases.

- Used Car Market Growth: New car shortages led many to the used car market, causing a surge in demand and subsequently, in prices.

How to Navigate Negative Equity

For those faced with negative equity, some strategies might help:

- Hold onto the Car: One of the simplest solutions is to keep the vehicle until the equity position improves.

- Refinance: If possible, refinancing the loan for a better interest rate or longer term can help manage monthly payments.

- Make Extra Payments: By paying more than the monthly due, you can reduce the principal faster, aiding in recovering the equity position.

If You Have to Trade-In

Utilize Cash Rebates: There’s a silver lining! Manufacturers often offer cash rebates on new cars, which can be an effective tool to reduce negative equity. Applying these rebates directly to your loan balance can bring you closer to a positive equity position or at least reduce the negative gap.

If you’re looking for vehicles with the best cash rebates, check out our Best New Cars for Negative Equity page. It lists the new cars with the highest rebates, offering valuable insights to make an informed choice.

Wrapping It Up

Understanding the market dynamics and timing of car purchases is crucial in making informed decisions about vehicle financing. Buyers in the 2020-2023 window, especially those with low down payments, faced a unique set of challenges. Being aware of such trends and making plans accordingly can help navigate the often turbulent waters of auto financing.

AutoByPayment.com offers accurate estimates of new and used car loan payments based on self-selected credit score, current rebates, down payment, and trade equity or negative equity, without customers having to provide their personal identifying information such as email and phone.