When it comes to buying a new car, understanding the various new car pricing terms can be difficult. Two of the most commonly mentioned figures in the car-buying process are the Invoice Price and the Manufacturer’s Suggested Retail Price (MSRP), which can be found on the Monroney sticker. In this post, we will delve into the invoice price vs. the MSRP, as well as the items you can find on the manufacturer’s invoice and the Monroney sticker, to help you make an informed decision when purchasing your next vehicle.

MSRP: The Starting Point

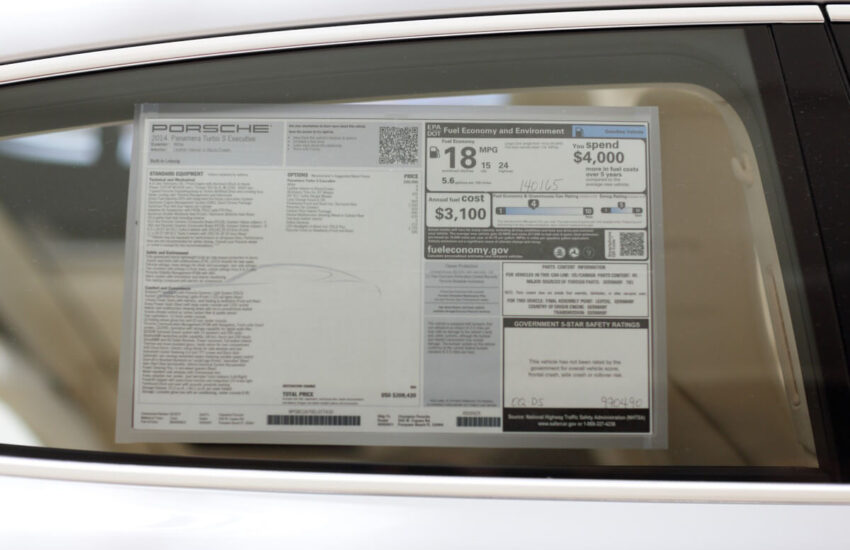

The Manufacturer’s Suggested Retail Price, often abbreviated as MSRP, is the price that the automaker recommends dealers charge for a particular vehicle model. The MSRP serves as the starting point for negotiations and is typically displayed prominently on the Monroney sticker, also known as the window sticker, which is affixed to the window of each new car for sale. The Monroney sticker includes essential information about the vehicle, such as its make and model, standard features, fuel economy ratings, safety ratings, and, of course, the MSRP. Their may also be an Addendum Sticker listing the price of dealership installed accessories. Be aware, however, that the window sticker and Addendum will not list the price of add-on items sold by the dealership finance office.

While the MSRP is a valuable piece of information, it’s important to remember that it’s essentially the manufacturer’s suggested price, and dealerships are not obligated to sell the car at this price. In fact, it’s quite common for buyers to pay less than the MSRP, especially when negotiating with the dealer.

Invoice Price: The Dealer’s Cost

The Invoice Price, on the other hand, is the amount that the dealership pays the manufacturer for each vehicle in their inventory. This price is not typically disclosed to the public, but dealerships use it as a reference point when negotiating with customers.

The Invoice Price includes several costs that the dealership incurs, such as the base cost of the vehicle, any optional add-ons or packages, and the destination charge (the cost of transporting the vehicle from the manufacturer to the dealership). Dealerships also receive incentives, rebates, and other discounts from the manufacturer, which can lower the actual amount they pay for the vehicle.

The Manufacturer Invoice: A Closer Look

The manufacturer’s invoice, which the dealer receives, contains a breakdown of the costs associated with the vehicle. It includes:

Base Price: This is the starting cost of the vehicle without any optional features or accessories.

Optional Equipment: Any additional features, packages, or accessories that the dealer has chosen to add to the vehicle. These can significantly increase the invoice price.

Destination Charge: The cost to transport the vehicle from the manufacturing facility to the dealership. This is typically a fixed fee.

Holdback: A manufacturer-to-dealer incentive where the automaker refunds a percentage of the vehicle’s MSRP to the dealership after the sale.

Advertising Fees: Some manufacturers charge dealerships for advertising and promotional materials.

Negotiating Beyond MSRP and Invoice Price

While both the MSRP and Invoice Price provide valuable information, savvy car buyers often negotiate a price somewhere between these two figures. Dealerships have some flexibility in pricing, and factors such as demand for the specific model, time of year, and dealership incentives can all influence the final sale price.

Additionally, it’s essential to be aware of any available rebates, incentives, or special financing offers that can further lower the price you pay. These incentives can vary by manufacturer and region.

Wrapping It Up

Understanding the difference between the MSRP, Invoice Price, and the items listed on the manufacturer invoice is crucial when purchasing a new vehicle. Armed with this knowledge, you can negotiate effectively and make a well-informed decision, ensuring that you get the best possible deal on your next car. Happy car shopping!

AutoByPayment.com offers accurate estimates of new and used car loan payments based on self-selected credit score, current rebates, down payment, and trade equity or negative equity, without customers having to provide their personal identifying information such as email and phone.